M&A Market Trends July 2023

posted 25th July 2023

M&A grows more popular every year, no longer exclusive to large companies, an increasing number of SMEs are joining them on both the buy-side and the sell-side. The market is driven by mid- and long-term trends, in July’s shared insight, we bring you some of the highlights in Dealsuite’s mid-market trends report 2023.

M&A is becoming more popular across companies of all sizes

Companies tend to strive for growth. M&A is the only alternative to organic growth. Almost all listed and large companies understand that in addition to organic growth, they should pursue strategic deals to maximise growth. Evidence shows that static portfolios underperform. In contrast, successful companies use M&A and selective divestitures to continually shift their portfolios towards a better future position (McKinsey). An increasing number of mid-market companies follow the example set by large corporates. They recognise the added value of M&A and include it in their growth strategy. Thus, more players are finding their way into the M&A sphere. As the number of PE companies also increases year by year, there will be more competition.

Market trends are more diversified

New situations, new types of companies and new types of leadership are changing the M&A sector. Acquiring 100% of the shares is no longer the obvious choice. Deal structures become diversified; deal engineering becomes innovative. These days, deals can result in anything from total integration to a light form of cooperation. They may start small but lead to stronger, broader cooperation in the future. Generally, newer types of cooperation are based on mutual interest. This makes sense as most businesses are ‘open to strategic opportunities’. With the diversification of deal structures, the Joint Venture model is gaining in popularity. In this setting the winners are those who discover how to help each other add value. Companies should look to find partners in business, rather than targets.

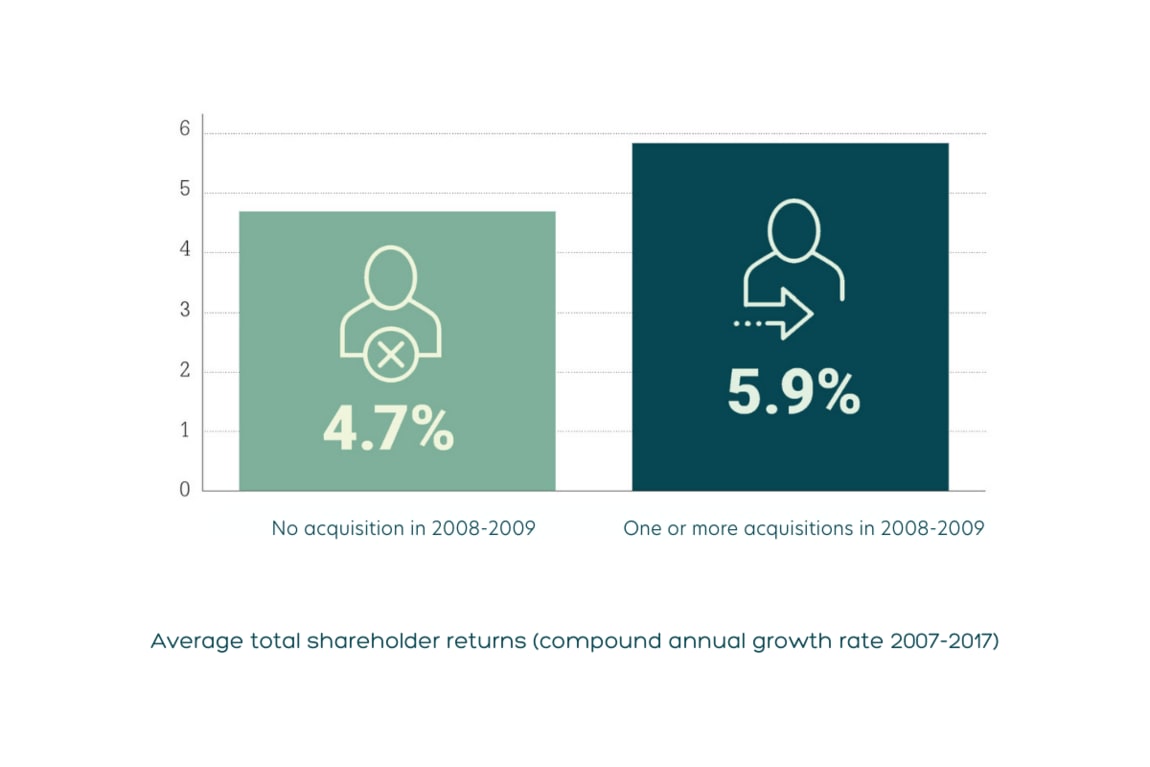

Active acquirers outperform in times of heightened economic volatility

Businesses typically respond to market downturns by pausing M&A. Convention suggests that it’s too risky to do deals when the economic outlook is uncertain and financing is harder, and this is reflected in M&A deal volumes. Recessions always lead to a drop in deals. But research shows that companies are wrong to be cautious. Looking at previous recessions reveals that consistent M&A activity through all economic cycles generates the highest returns. Companies that were active acquirers before the global financial crisis in 2008 performed best by staying active during the recession, according to research by as well Bain as McKinsey. Bain research reveals that these companies earned an average shareholder return of 6.1% during the decade from 2007, compared to a return of 3.8% for companies that were active pre-recession but moved to the sidelines during the crisis. The gap is even bigger when comparing companies that were inactive in M&A generally. PwC found a similar effect on returns. Just one year later, companies that had completed acquisitions during the recession in 2001 out-performed the overall sector by double digits.

‘Scope deals’ are more popular than ‘scale deals’

Companies that want to realise a greater presence in a particular market or sector and aim to achieve a greater overall economy of scale, may opt for a scale acquisition. In this case, the target is typically a competitor or a company in a related sector or a new geographic market. With scope deals, companies seek new capabilities and access to new markets or other complementary services. In 2018, ‘scope’ for the first time outranked ‘scale’, accounting for 51% of global M&A activity (going up from 41% since 2015). In 2019, it already went up to 58%. An increasing number of buyers were looking to expand their capabilities through acquisitions. In 2018, ‘scope’ for the first time outranked ‘scale’, accounting for 51% of global M&A activity (going up from 41% since 2015).

Companies develop their M&A brand

Leading companies manage and develop their M&A brand and reputation (McKinsey). These companies do not solely rely on the pull of their brand (which they tend to overestimate), but complement it with a rigorous and thoughtful process for finding new acquisition targets (Bain). Only by being top-of-mind in the minds of sellers and sell-side advisors, companies can avoid missing out on opportunities. It also needs to be easy for sellers and advisors to get in touch with the right person in your company. Obviously, your company is often unknown to sellers in adjacent industries and geographies. With the convergence of industries, it becomes crucial for sellers to be aware of your company’s interests. Especially with the high volume of companies in the mid-market. Therefore, it is vital to present your M&A team and your strategic ambitions to the community. In this way, the M&A brand serves as pull marketing.

Digital M&A is here to stay

M&A is generally perceived as a conservative sector. That conservatism is mostly due to the high stakes that are involved. That also showed when it comes to the adoption of digital transformation. However, digitalisation has now been around in M&A for over a decade. Early adopters have profited from competitive advantages. And though culture doesn’t change overnight, we can safely assume that digitalisation is here to stay. The pandemic had already increased the importance of digitally supported work processes, now the geopolitical tensions further emphasised this. Digital support offers several benefits in times of changing circumstances:

• Remote and efficient deal execution

• Enhanced due diligence

• Increased information security

• Improved collaboration and communication

• Agility and adaptability

M&A remains a personal business but will be heavily supported by technical solutions

Face-to-face meetings have become less common after the Covid-19 outbreak, and the number of personal interactions in M&A will not return to pre Covid levels. Yet, there is obvious value in looking a deal partner in the eye during negotiations and in situations when emotions can run high. Technological support is here to stay, especially in the earlier stages of the deal process. We will move forward with a hybrid model: personal dealmaking, aided by technical solutions. Or to formulate it as an advice: For corporate M&A to stay competitive in the ‘20s they should move forward with a human-led, data driven and technology-powered approach.