Fuelling Employee Ownership: Demystifying the Funding of EOTs

posted 23rd June 2023

Employee Ownership is becoming an ever more popular form of business sale, where shareholders sell a controlling stake (at least 51%) to employees of the business. The price is based on an independent assessment and agreed at market value. Employee Ownership Trusts offer a compelling alternative for business owners who want to pass on their legacy, empower their employees, and ensure the long-term sustainability of their companies.

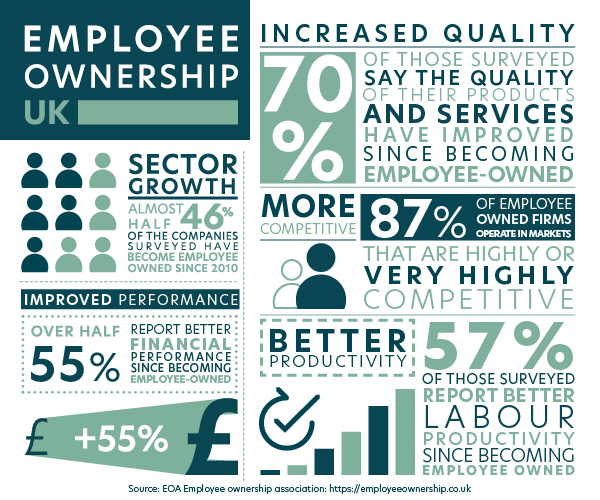

With over 1,030 businesses (and rising) now employee-owned in the UK, the option to sell your business to your employees is one that has gained significant attention – and for good reason. Boasting potential benefits such as increased sales and an upsurge in productivity from employees due to incentives for success and a tangible tie to the business, Employee Ownership has become most popular in the Professional Services, Construction, Manufacturing, Retail and Wholesale, and Information and Communications sectors.

Find out exactly how an EOT works, and the potential benefits it could bring, in our short video here.

You can also read more about the benefits of an EOT in our Shared Insight post here or take a peek behind the deal of some of the Employee Ownership transactions we've supported here.

But how is an Employee Ownership transaction funded? Do the employees need to buy the shares? Understanding how EOTs are funded is crucial for both owners considering this transition and employees curious about their financial future.

Sources of Funding for Employee Ownership Trusts

1. Cash Flow from Operations: A sustainable and profitable business generates cash flow, which can be used to fund an employee ownership transaction. Companies with robust cash flows can choose to assign a portion of their profits (after tax) as payment for the shares the owner has sold to the employees. The Employee Ownership Trust holds the shares on behalf of the employees and will also manage the payment to the owner in instalments.

This method is often preferred when the business has consistent earnings, and the owner has the flexibility to transition gradually.

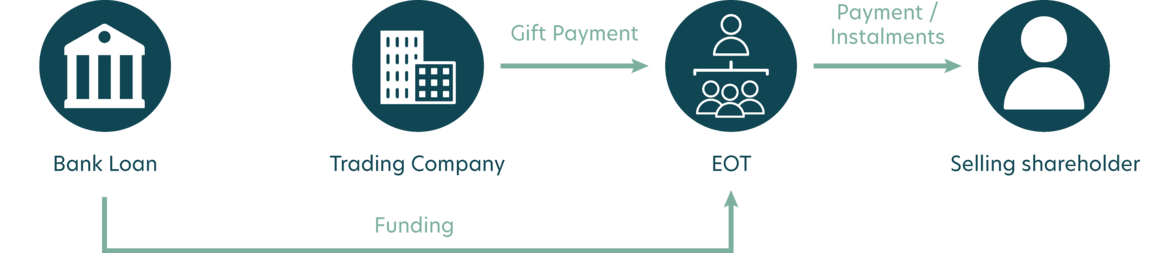

2. Debt Financing: In some cases, a business might choose to leverage debt to fund an employee ownership transaction by obtaining a loan to finance the purchase of shares from the shareholder(s). The loan can be obtained through the trading company or the EOT.

If the loan is obtained through the company, the lender provides funds directly to the trading company, and the trading company then gives these funds to the trust. The EOT then handles paying this initial consideration to the selling shareholder. The loan repayments are then made by the trading company from future profits (after tax).

If the loan is obtained directly by the EOT itself, the trust uses this funding (and any payment from the trading company if applicable) to provide the initial consideration to the selling shareholder. To repay the loan, the trading company regularly provides the trust with a portion of profits (after tax), which is then paid to the lender in instalments.

Whether the funding is provided to the trading company or directly to the trust, it is important to carefully evaluate the company's ability to service that debt and ensure that the trust's financial obligations are manageable.

3. Seller Financing: In situations where the business owner is open to providing financing, they can opt for seller financing. This arrangement allows the owner to receive payments over time from the trust in exchange for the shares. It provides a flexible option for funding an EOT while ensuring a smooth transition and potentially favourable terms for both parties involved.

Tax Advantages of Employee Ownership Trusts

One of the significant benefits of employee ownership is the potential tax advantages they offer. Following the introduction of Employee Ownership Trusts by the UK Government in 2014, there is a considerable incentive for employers to sell their shares to employees. If the sale and company are structured correctly, shareholders will pay 0% capital gains tax when selling their shares to employees. These shares are also exempt from Inheritance Tax Transfer.

Additionally, following the transaction, the employees will be able to receive a bonus of up to £3,600 free of income tax and the EOT may also benefit from relief from IHT principal charges and exit charges.

These tax incentives can enhance the attractiveness of EOTs as a succession planning tool while supporting the business owner's financial goals.

Ultimately, an Employee Ownership transaction can be funded through several avenues, and the completion of the transaction will depend on the seller's situation and the company's goals.

GS Verde Group has guided many businesses through successful Employee Ownership transactions; where our multidisciplinary approach allows us to provide support in deal structuring, due diligence, heads of terms, trust set-up, and funding. With access to a comprehensive pool of funders across the UK & Ireland, GS Verde can advise on which funding options are open to you and how they might benefit the business and the transaction overall.

Find out more about Employee Ownership here or read about some of the businesses GS Verde has supported on their Employee Ownership journey here.

The GS Verde Group are business-focused experts in getting deals done. The group combines multiple disciplines including law, tax, finance and communications, to provide end-to-end support as a complete advisory team.